One of the most important payment innovations that we are likely to see over the next two or three years is the birth of instant payments in Europe. Although similar payment schemes already exist in individual countries such as UK (Faster Payments) and Singapore (Fast and Secure Transfers – FAST), Denmark (express transfers) and Australia (in development), the introduction of instant payments across the Eurozone will revolutionise payments across 338.3 million people and 19 countries. BNP Paribas is leading innovation and driving momentum in instant payments, recognising that instant payments represent a once-in-a-decade opportunity to improve customer satisfaction, reduce cost and fraud, and revolutionise both established and emerging sales models.

Defining instant payments

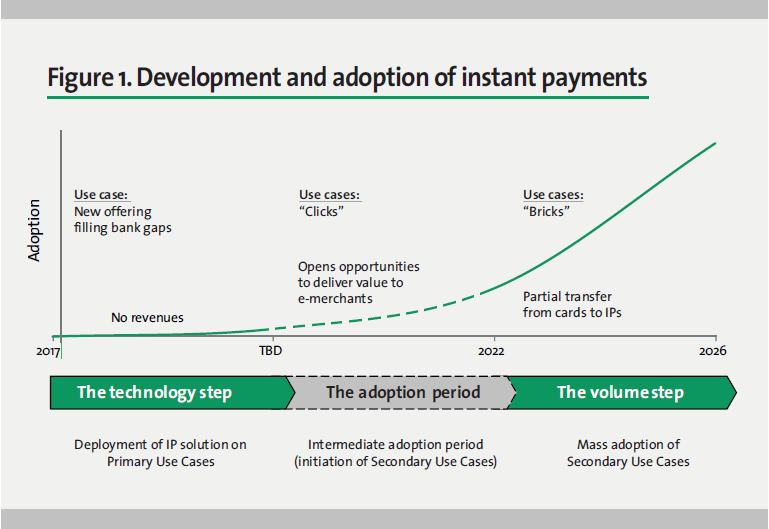

When we refer to ‘instant payments’, we are discussing payments that can be made 24/7, with immediate transfer of value, credit to the payee’s account and ability to re-use funds. The two parties to a transaction are informed straight away that a transaction has, or has not been successful, enabling the goods and services to be transferred, and credit limits freed up. Real-time, 24/7 payments are no longer an aspiration but an expectation for both consumer and wholesale payments, and there is considerable motivation amongst payment providers (both banks and non-bank payment service providers or PSPs), users and regulators to deliver on this expectation. The question, however, is how we get there, given the scale of undertaking and disruption to existing payment and collection processes. Therefore it might be interesting to see how the uptake took place (or is still taking place) in the instant payment schemes already in place. Like every major industry undertaking, the development of instant payments is likely to take place through a number of distinct phases (figure 1).

Phase One. Investment and co- creation

First is the technology stage. This is the design and delivery of instant payment solutions, in combination with pilot clients. While some PSPs already offer solutions that enable instant payments, banks do not, so the technology stage will require substantial investment in supplementing and re-designing products.

This is an essential development for the banking industry that has a strategic commitment to remaining clients’ trusted partner for payment services, and both consumers and institutions can expect to see new solutions relatively quickly. In the Eurozone, for example, with the European Payments Council due to deliver the scheme for instant payments in November 2016, we can expect the first Euro-based pilot clients to be live on new instant payment solutions in the latter part of 2017.

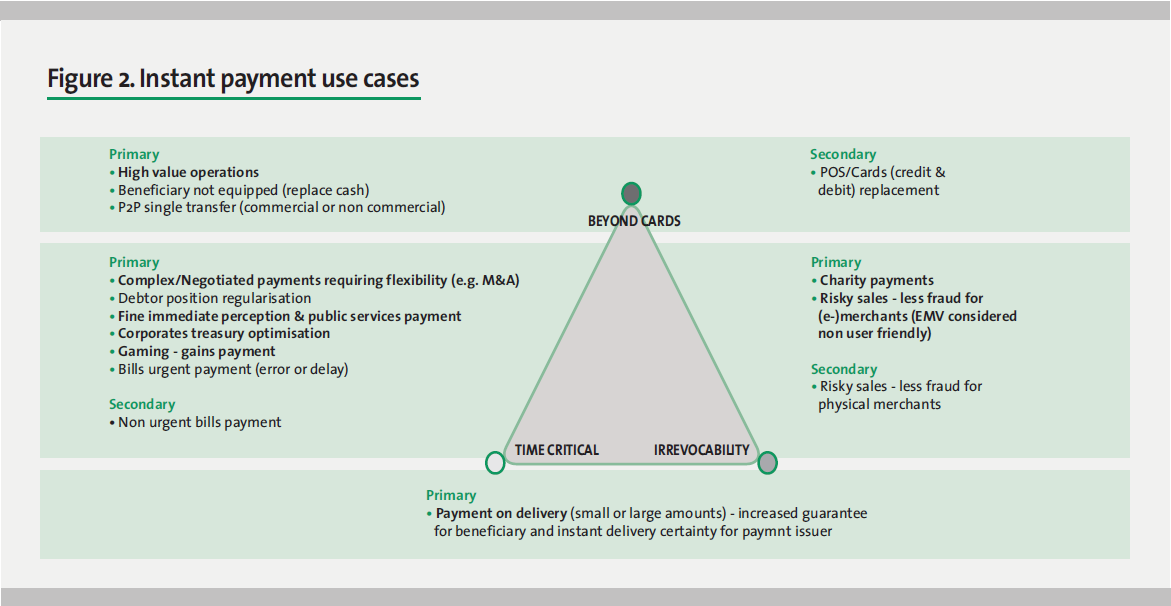

Having modelled a variety of use cases (figure 2), we have identified three key areas in which instant payments can bring value:

Universal access

While cards will continue to be a very useful payment method, as this article discusses, due to the credit element and convenience in particular, instant payments offer value in situations where cards cannot be used. They will also offer an alternative to cards in countries and amongst consumers for whom cards are less prevalent. For example, purchasing high value items is often not possible due to restrictions on credit limits and transaction sizes. A second problem is that while card payments are feasible between consumers and businesses that accept cards, they cannot be used to make payments between individuals or small businesses who cannot, or for whom it is not cost-effective to accept cards. In these situations, instant payments will play a valuable role, with the benefit that they are accessible to consumers and businesses.

Immediacy of payment

Today, the advantage of paying by cash or card is that they offer immediacy of payment and/or payment guarantee, so a buyer can leave a store with the item they have purchased. This is not currently the case with electronic transfers and as a result, they are not suitable for many types of transactions that require payment on delivery. This problem applies at a corporate as well as a consumer level, which is one of the factors that leads companies to use letters of credit and other trade finance instruments.

Irrevocability

According to our research, payment finality is the most important feature that instant payments can offer, and which can make them more attractive than cards for many retailers. This is not currently a solution provided by banks, but when combined with immediacy of payments, instant payment solutions will prove a powerful offering to support both B2B and B2C payment-on- delivery sales models.

Phase Two. A complement to e-commerce

Once new instant payment solutions have been developed and piloted with co-creation clients, there are certain industry segments that are likely to be early adopters, such as e-retailers. These companies are most likely to add instant payments along sidecards, PayPal etc., as acomplementary payment method, rather than replacing thesemethods.

However, given the rate of growth in e-Commerce that we are witnessing, which will inevitably result in higher rates of useof both instant payments and cards, weexpect therate of growth in instant payments to increase beyond that of other e-Commerce payment methods. This early adoption period will be crucial for banks by commercialising solutions that have been co-created and piloted with key customers, and refining the business case for different industries and business models.

Phase Three. From ‘clicks’to ‘bricks’

The trigger for mainstream, rather than early or niche adoption, is likely to be the use of instant payments by ‘bricks and mortar’ as well as e-Commerce businesses. This represents the most significant step in adoption, as these businesses will need to restructure their technology and sales processes, including both point of sale and back-end systems, to accept instant payments. As with e-retailers, instant payments are unlikely to replace existing payment methods in most cases, but just as many companies now discourage the useof cash and manual payment instruments such as cheques, the convenience, immediacy and low cost of payments is likely to prove attractive. While cards offer a similar level of convenience, the relatively high levels of cost, including production costs, interchange fees, high costs associated with fraud and payment terminalfees, are likely to encouragetheuseof instant payments as an alternative; however, thecredit component and worldwide acceptance, including for cross-border payments, will ensure that cards continue to co-exist with instant payments.

Innovation and investment

Given the strong push from the ERPB (Euro Retail Payments Board, which replaces the SEPA Council), instant payments will become a reality very quickly. Leading banks, such as BNP Paribas, are working actively with the European Payments Council to develop an SCTInst scheme (a standardised instant payments scheme for SEPA credit transfers) which will therefore create opportunities on a pan-European basis. At the same time, banks and other key stakeholders are co-operating closely in individual markets, and most clearing systems have announced that they are developing an instant payments proposition. What is critical is that these solutions start from a clear usecase definition and therefore satisfy specific needs of the user community. As a result, defining detailed use cases with user communities, both for domestic and cross-border payments, is an essential activity in which BNP Paribas is engaged. In some cases, these use cases can be used to define proprietary solutions, and therefore do not require wider collaboration, but more often, there needs to be a critical mass of participants at an interbank level to bring solutions to market. By creating momentum in these discussions, and translating discussion into consensus, the development process will accelerate. There are still a number of questions to be answered, not least the countries in which instant payment solutions will next materialise and when, and the opportunities for collaboration across countries and clearing systems, but the direction is clear. Furthermore, the commitment of banks such as BNP Paribas which are taking a pioneering and proactive role is essential to pinpoint the specific needs of payment users, develop the solutions that will meet their expectations, and drive an efficient and robust payments industry